Batch Month-End Credit Card Payments to Suppliers with 70% Touch Time Reduction

Dec 19, 2025

Month-end supplier payments don’t need to take days. This guide shows how Australian businesses and bookkeepers batch credit card payments to cut touch time by up to 70%, unlock up to 55 days of float, and auto-reconcile in Xero and MYOB—using Lessn, even when suppliers don’t accept cards.

This article explains how batching month-end credit card payments to suppliers can reduce touch time by up to 70 percent, streamline approvals and reconciliation, and unlock cashflow and rewards for Australian SMBs and bookkeepers.

What you’ll learn:

How batch month-end credit card payments work compared to traditional supplier payment workflows

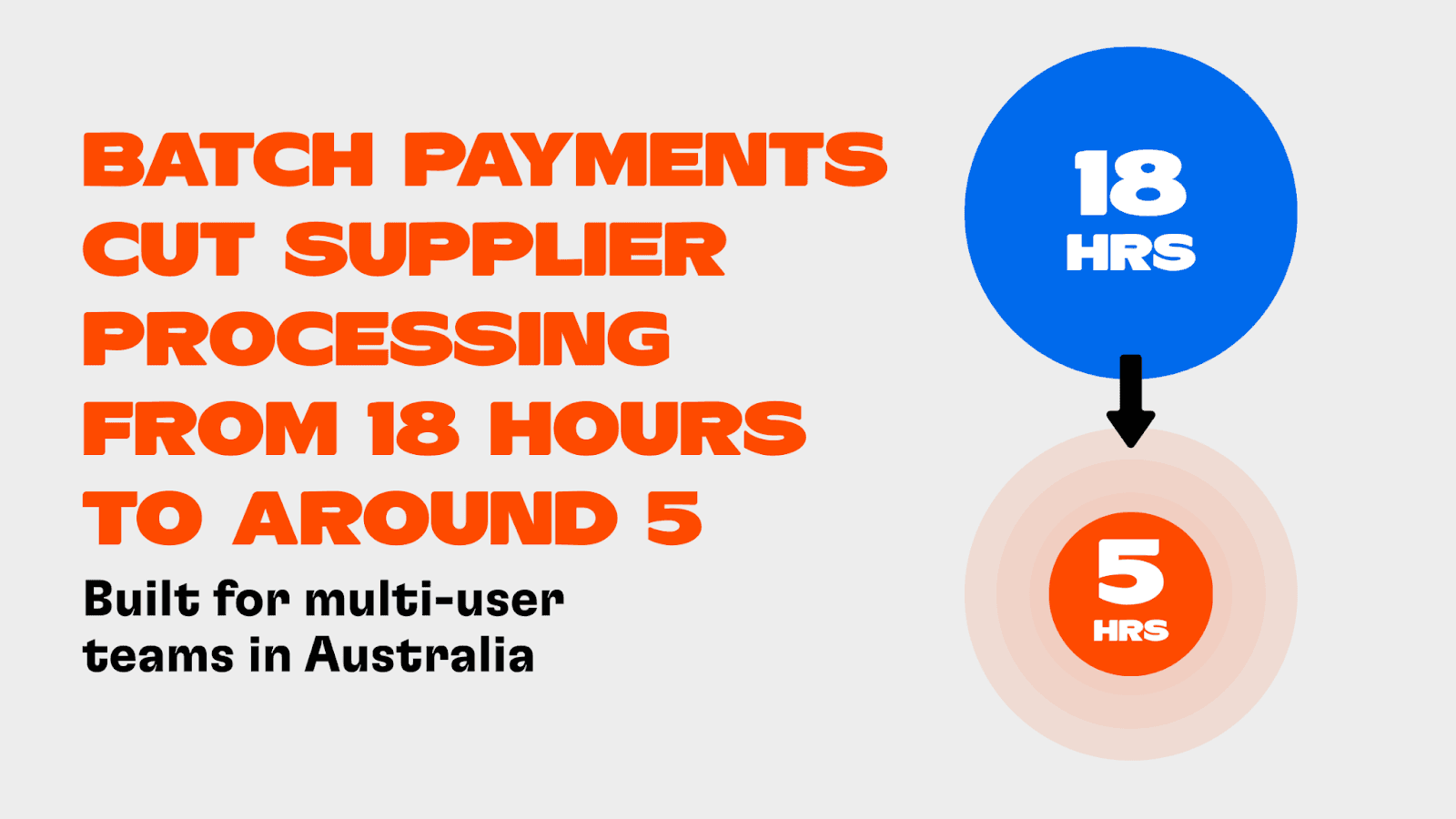

Why manual month-end processing costs up to 18 hours per week in admin time

How batching reduces touch time to around 5 hours while improving visibility and control

How to fund supplier payments via Amex, Visa, or Mastercard even if suppliers do not accept cards

How automatic reconciliation in Xero, MYOB, and QuickBooks eliminates manual clean-up

How batching supports compliance ahead of the 2026 $10,000 cash mandate

How credit card float, rewards, and early payment discounts improve working capital

Month-end is where most Australian businesses and bookkeepers lose time, visibility, and patience.

Invoices arrive through emails, portals, PDFs, and spreadsheets. Supplier payments are handled one by one. Approval chasers start. ABA files are rebuilt. Reconciliation drags into the following week. For many SMBs, month-end supplier payments consume up to 18 hours every week, often across several people, with high risk of error and little financial upside.

This problem is not caused by complexity in the business. It is caused by fragmented payment workflows.

Batch month-end credit card payments to suppliers change this completely. Instead of processing dozens or hundreds of invoices individually, businesses group them into a single batch, approve once, fund via credit cards, and pay suppliers by standard bank transfer.

The result is a documented 70 percent reduction in touch time, from around 18 hours per week to closer to 5 hours, while also unlocking rewards, early payment discounts, and extended cashflow.

Platforms like Lessn make this possible even when suppliers do not accept cards. Businesses fund payments using Amex, Visa, or Mastercard. Suppliers receive next business day EFT or BPAY. Accounting systems like Xero and MYOB reconcile automatically. Merchant fees are journaled without manual work.

This guide explains how batch month-end credit card payments suppliers Australia work, why they matter ahead of the 2026 cash mandate, and how Australian SMBs and bookkeepers are using batching to reduce admin, improve cashflow, and scale without adding headcount.

What Are Batch Month-End Credit Card Payments?

Batch month-end credit card payments are a way to process large volumes of supplier invoices through a single workflow rather than handling each payment individually.

Instead of approving and paying invoices one by one, finance teams group multiple unpaid invoices into a batch. That batch is approved once, funded via one or more credit cards, and then paid out to suppliers by standard bank transfer. From the supplier’s perspective, nothing changes. They receive EFT or BPAY into their bank account. From the business perspective, the workflow is dramatically simplified.

The key difference between batch payments and traditional supplier payments is consolidation.

Traditional month-end processing involves multiple touchpoints. Each invoice is reviewed separately. Approvals are chased manually. Payments are scheduled individually. Reconciliation happens line by line. Merchant fees are matched manually across dozens of transactions.

Batch processing replaces this with a single flow.

Invoices are bulk uploaded from Xero or as PDFs and emails. Optical character recognition extracts amounts, suppliers, and due dates automatically. One approval workflow covers the entire batch. Funding is split across multiple cards if required. Suppliers are paid in one scheduled run. Reconciliation happens automatically back into Xero, MYOB, or QuickBooks.

For example, a business with 75 suppliers and a total month-end bill run of $75,000 can upload all invoices on day 25, approve once on day 28, fund the batch on day 30, pay suppliers on day 31, and close reconciliation by day 32. The entire cycle is predictable, controlled, and traceable.

This is why batch supplier payments Xero Australia has become a critical workflow for modern finance teams.

Why Australian SMBs Need Batch Processing in 2026

Batch processing is not just about saving time. It is increasingly about compliance, cashflow, and risk management.

Manual month-end is breaking finance teams

Around 68 percent of Australian SMBs still rely on manual approval methods for supplier payments. Email chains, spreadsheets, and ABA files remain common. These methods introduce delays, increase fraud exposure, and make audits painful.

Manual month-end processing typically involves 12 to 18 hours of touch time per week. This includes invoice chasing, approval follow-ups, payment scheduling, reconciliation, and corrections. It also increases the chance of duplicate payments or missed invoices.

The 2026 cash mandate accelerates the shift

From January 2026, businesses will no longer be able to make or accept cash payments over $10,000. Supplier payments must be digital, traceable, and auditable. Batch credit card payments with EFT payouts meet this requirement cleanly.

Each batch creates a complete digital trail from invoice upload to supplier receipt. Approval records, funding sources, and reconciliation logs are stored automatically. This reduces compliance risk and simplifies ATO and AUSTRAC reviews.

Financial upside compounds quickly

Batch processing delivers benefits that individual payments cannot match.

Manual individual payments require separate transactions, separate approvals, and separate reconciliation entries. Batch payments apply a single approval and a single workflow across the entire volume.

The impact is significant:

Manual individual processing averages around 18 hours per week

Batch credit card processing reduces this to around 5 hours

Manual payments offer no card float or rewards

Batch credit card payments unlock up to 55 days interest free float

Manual reconciliation is error prone

Batch reconciliation is automatic in Xero and MYOB

For bookkeepers, this efficiency allows them to manage up to four times as many clients without increasing staff.

How Batch Month-End Payments Work Step by Step

Batch processing follows a structured timeline that aligns with how finance teams already work at month-end.

Preparation on day 25

On or around day 25, unpaid bills are exported from Xero or MYOB. Invoices may also be added via bulk PDF upload or forwarded from email. Optical character recognition extracts supplier names, invoice amounts, and due dates automatically.

For a typical batch, this might include 75 invoices totaling $75,000 across 75 suppliers.

Approval on day 28

Rather than approving each invoice individually, the entire batch moves through a single approval workflow.

Parallel approvals can be used for speed, such as operational approvals for invoices under $5,000. Sequential approvals can be applied for larger invoices, such as director sign-off for payments over $50,000.

Approvers receive mobile notifications and complete approvals using two-factor authentication. Notes can be added for context. Individual invoices can still be rejected or edited without breaking the batch.

Funding on day 30

Once approved, funding is allocated across one or more credit cards. Lessn supports automatic card splitting to manage headroom and maximise rewards.

For example, 40 percent of the batch may be funded via a NAB Rewards card, with the remaining 60 percent funded via an Amex Platinum card. This avoids hitting card limits while optimising points earned.

Execution on day 31

Suppliers are paid via next business day EFT or BPAY. Suppliers receive payments as usual and do not need to accept cards.

Merchant fees, such as 1.50 percent plus GST on Visa, are automatically posted to the ledger as part of the batch.

Reconciliation on day 32

Payments are automatically reconciled back into Xero, MYOB, or QuickBooks. Each invoice is marked as paid. Merchant fees are journaled correctly. An immutable audit trail is created and stored.

The entire month-end cycle is closed within a predictable window, without manual clean-up.

Quantified Benefits and ROI

Batch processing delivers measurable returns that compound over time.

Time savings

A 70 percent reduction in touch time means approximately 13 hours saved per week. At $15 per hour, this equals around $780 per month per user.

Cashflow improvement

Batch payments funded via credit cards unlock up to 55 days of interest free float. When suppliers are paid on day 30 and cards are settled on day 55 from the next cycle, businesses effectively extend working capital without delaying suppliers.

Rewards and discounts

A $75,000 batch funded on cards earning 2 points per dollar generates 150,000 points. Early payment discounts of 2 percent on the same batch save an additional $1,500.

Risk reduction

Batch workflows with approvals, two-factor authentication, and audit trails reduce accounts payable fraud risk by up to 85 percent.

Combined, these benefits deliver an estimated 300 percent return on investment in the first year.

Real-World Use Cases

A tradie business processing $50,000 per month batches suppliers like Bunnings, Wesfarmers, and Telstra. By batching payments and splitting across ANZ and CommBank cards, they save 15 hours per month and earn over 100,000 Qantas points annually.

A bookkeeping agency runs ten separate client batches from one dashboard. Client-specific rules prevent cross-entity errors. Weekend escalation ensures payments do not stall.

An importer processes 100 FX line items totaling $100,000. Batch processing routes payments through compliant FX workflows with full AUSTRAC audit logs and next day settlement.

Batch Payments vs Traditional Methods

Manual ABA files require high touch time, offer no float, and rely on basic compliance controls.

Individual card payments improve float but still require multiple approvals and partial reconciliation.

Batch credit card payments reduce touch time to around 5 hours per week, unlock full rewards, automate reconciliation, and create AUSTRAC-ready audit trails.

This is why credit card batch payments reduce touch time so dramatically compared to legacy methods.

Implementation Best Practices and Challenges

Start with a small pilot of ten invoices to build confidence. Move to a weekly or monthly batch cadence. Monitor card headroom using dashboards and auto-splitting.

Common concerns around card limits, disputes, or supplier resistance are largely unfounded. Suppliers receive standard EFT. Individual invoices can be edited or rejected before execution. Training typically takes around fifteen minutes.

Track batch growth, approval times, and rejection rates to ensure workflows remain efficient.

Conclusion

Batch month-end credit card payments transform supplier payments from a chaotic, manual process into a predictable, automated workflow.

By consolidating invoices, approving once, funding via cards, and reconciling automatically, Australian businesses and bookkeepers reduce touch time by up to 70 percent while improving cashflow, compliance, and rewards.

Lessn enables this at scale, even when suppliers do not accept cards.

If month-end still takes days, it is time to batch it.

Start batching supplier payments with Lessn today.

Frequently Asked Questions about Batch Month-End Credit Card Payments to Suppliers

How much time does batching save?

Batch processing reduces touch time by around 70 percent, from approximately 18 hours to about 5 hours per week.

Can suppliers who reject cards still be paid?

Yes. Suppliers receive standard EFT or BPAY while the business funds payments via credit cards.

Does Xero auto-reconcile batch credit card payments?

Yes. Invoices, payments, and merchant fees are automatically matched.

Which cards work best for batch payments?

Amex Platinum, NAB Rewards, and CommBank Smart Awards are commonly used.

Is batch processing AUSTRAC and ATO compliant?

Yes. Full audit trails and digital records are created for every batch.

Continue Reading

START REWARDING YOUR HARD WORK TODAY

Join Australian businesses turning payments into rewards.