Multi Client Supplier Payments Bookkeeper: Card Splits vs Single Bank Account

Feb 25, 2026

Seven clients processing $120,000 a month is where most bookkeepers hit a wall. A single bank account drains cash on day one, creates reconciliation risk across multiple ledgers, and caps growth at seven clients because accounts payable simply takes too long. By contrast, a card split model turns the same $120,000 batch into 55-day float, automated Xero multi-client reconciliation, and more than $2,000 in monthly net rewards. Platforms like Lessn allow bookkeepers to fund supplier payments across multiple cards while keeping each client entity clean, isolated, and audit-safe. For a modern multi-client supplier payments bookkeeper, card splits vs a single bank account is no longer a preference — it’s the difference between being stuck at seven clients or scaling to 25+ without adding admin hours.

This article explores the strategic difference between using a single bank account and card splits for multi-client supplier payments, showing how bookkeepers can unlock float, rewards, automation, and scalable growth across multiple property or trade clients.

What you’ll learn:

Why the single bank account model creates cash drain, reconciliation overload, and scaling limits

How card splits across multiple credit cards enable 55-day float per client

The real ROI comparison between $120,000 monthly via bank vs card-funded batching

How Xero multi-client auto-reconciliation eliminates manual ledger matching

How to maintain clean client entity separation and reduce audit risk

How rewards and early float can generate $2,000+ monthly net upside

7 Clients, $120k, and a Scaling Wall

If you are a bookkeeper managing multiple property or trade clients, you already know the pressure of month-end.

Seven clients can easily mean $100,000 to $120,000 in monthly supplier payments. Maintenance invoices. Utilities. Cleaners. ATO instalments. Contractors. Super. All flowing through one operating account.

Most bookkeepers still rely on a single bank account model. Money lands. Bills get paid. The account drains. Reconciliation begins. It works, but it caps your growth.

Here is the uncomfortable reality.

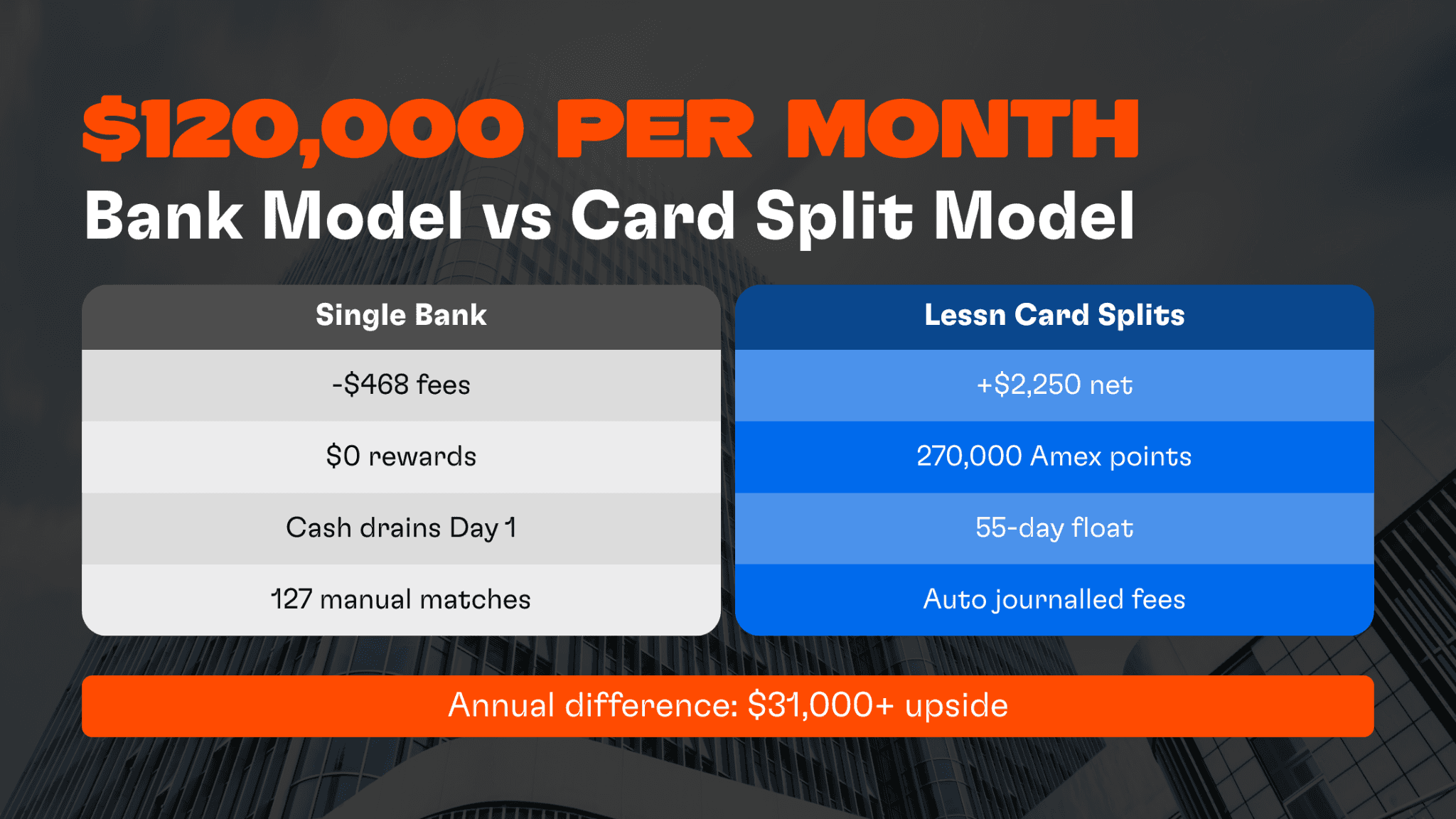

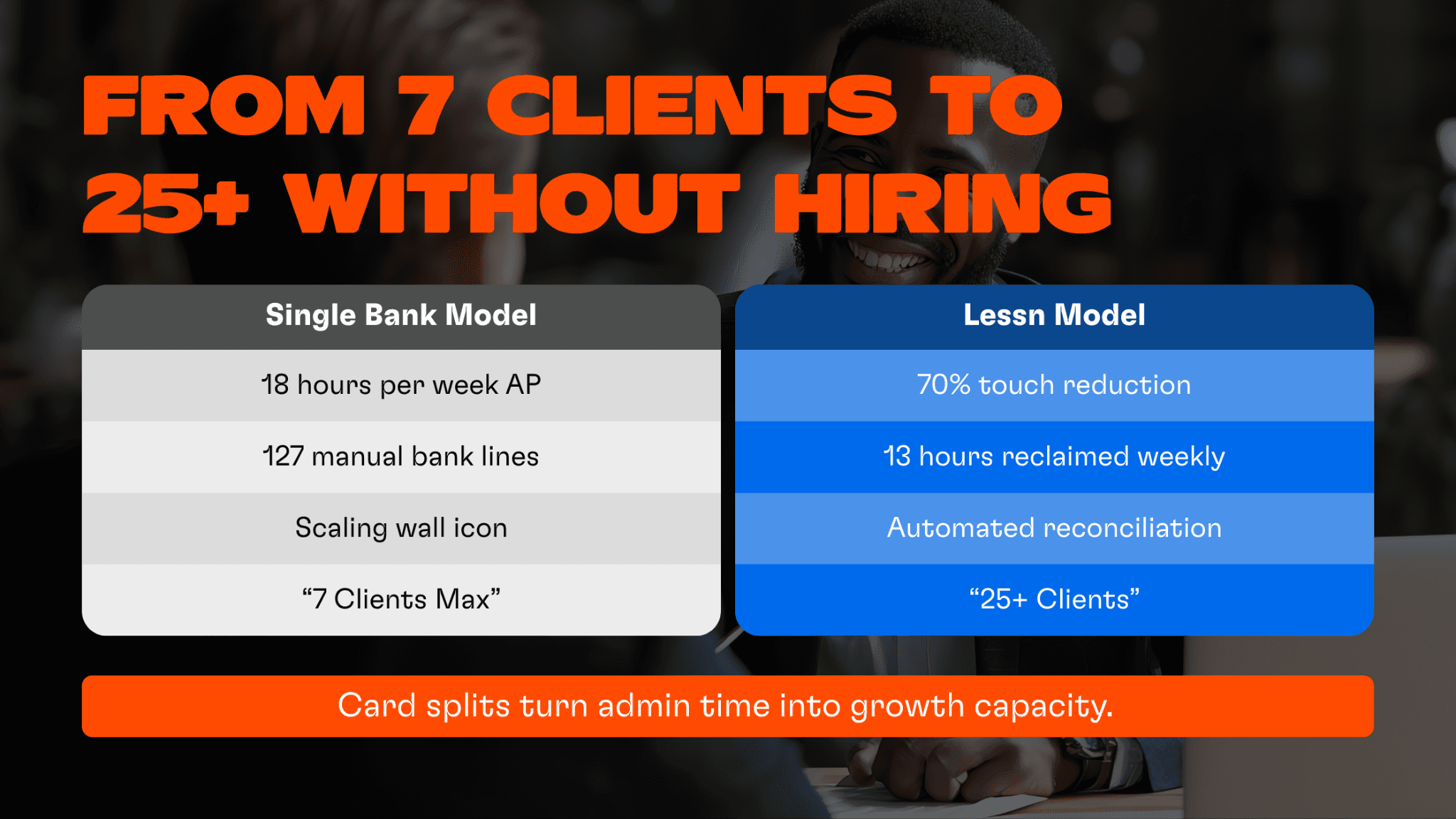

Seven clients processing $120,000 per month across 127 invoices can consume 18 hours per week in accounts payable admin. Cash leaves on day one. Bank fees apply. No float. No rewards. Manual matching across seven ledgers. You hit a ceiling at seven clients because you simply do not have the time.

Now compare that with a card split model.

The same $120,000 batch split across 10 credit cards delivers 55-day float, $2,000 plus monthly net rewards, automatic Xero multi client payment reconciliation, and a 70 percent touch time reduction. Instead of draining your operating buffer, the system funds itself.

This is where the debate of card splits vs single bank account becomes strategic rather than operational.

For a modern multi client supplier payments bookkeeper, the question is no longer whether batching works. It is whether you are leaving money and scale on the table by sticking with a single bank account.

The Single Bank Account Multi-Client Nightmare

Let’s walk through Jane’s reality.

Jane manages seven property clients. Total monthly supplier payments: $120,000.

Client A: $30,000 in Wesfarmers and Bunnings maintenance

Client B: $25,000 in cleaners and plumbers

Client C: $18,000 in utilities

Clients D to G: $47,000 across ATO, super, and contractors

Total: 127 invoices per month.

Day One Cash Drain

The first problem is immediate.

On payment day, $120,000 leaves the operating account. Instantly.

There is no float. No working capital buffer. No reward upside. Even at a low 0.39 percent transaction cost, that is $468 in pure expense with zero return.

Cash is gone. Buffer is reduced. If Client A runs heavy maintenance, Client B may experience pressure because the same bank account absorbs the load.

Mixed Ledgers and Audit Risk

With one bank account, all seven clients flow through the same source account. Even if you separate via tracking categories in Xero, errors happen.

A $30,000 Client A payment posted against Client B’s ledger can create reporting chaos. During ATO audits or BAS reviews, this mixing becomes risky.

This is the core weakness of single bank account vs multiple cards business models.

Manual Reconciliation Hell

127 invoices means 127 bank lines to match. Each with potential merchant references, rounding differences, and manual coding.

Multiply that across seven clients and you have a weekly reconciliation backlog.

Even experienced bookkeepers lose 10 to 15 hours per week here.

Scaling Wall

At 18 hours per week for accounts payable, Jane cannot realistically add an eighth client without sacrificing quality.

This is the invisible ceiling most multi-client bookkeepers hit.

The single bank account model works until it does not.

Lessn Card Splits: Multi-Client Workflow at Scale

Now let’s look at the same scenario using card splits.

Step 1: Bulk Upload and Client Separation

Jane uploads 127 PDFs via email. OCR extracts supplier names, invoice numbers, amounts, and assigns them to the correct client entity in Xero.

Each client dashboard remains separate. No ledger mixing. No cross-posting.

This is where bookkeeper credit card supplier payments Australia shifts from manual to automated.

Step 2: Client-Specific Rules

Client A might allow automatic approval under $5,000.

Client B might require director SMS approval above $25,000.

Client C might have strict ATO routing rules.

All configured per client.

Each entity remains isolated inside its own approval framework.

Step 3: 10-Card Split Dashboard

The $120,000 batch is allocated across 10 cards.

Example allocation:

40 % to Amex Platinum

30 % to NAB Rewards

20 % to CommBank Smart Awards

10 % to backup Visa

This avoids maxing limits and maximises reward optimisation.

Card splits allow each client to maintain effective float independently, even if funding ultimately flows from the same bookkeeper’s oversight.

Step 4: Single Approval, Multiple Clients

Invoices under $5,000 are approved in bulk.

Invoices over $50,000 trigger director SMS approval.

One consolidated workflow replaces 127 micro-decisions.

Step 5: Auto-Reconciliation per Client Ledger

Merchant fees are auto-journalled.

Amex at 1.95 percent

Visa at 1.50 percent

Each fee posts directly to the correct client ledger.

No manual coding. No reconciliation backlog. No cross-client errors.

This is true Xero multi client payment reconciliation.

ROI Math: When Cards Win

Let’s examine the numbers.

$120,000 Monthly Across Seven Clients

Cards via Lessn:

Rewards:

270,000 Amex points

At 1.7 cents per point = $4,590 value

Fees:

1.95 percent average = $2,340

Net monthly gain:

$2,250 plus 55-day float per client

Single Bank Model:

Fees:

0.39 percent = $468

Rewards:

$0

Net position:

-$468 with immediate cash drain

Twelve-Month Projection

Cards:

$2,250 monthly gain

$27,000 annual profit

3.24 million points accumulated

Single bank:

$5,616 annual cost

No rewards

No float

Over twelve months, the delta exceeds $31,000.

And that excludes time savings.

This is where credit card float multi client cashflow benefits becomes measurable rather than theoretical.

Real Multi-Client Bookkeeper Stories

Sarah: 12 Property Clients

Sarah scaled from seven to twelve property clients.

Monthly volume: $280,000.

Using card splits, she generates approximately $6,000 in monthly net rewards. That revenue funded a virtual assistant to handle onboarding and reporting.

Under a single bank account model, she would have needed multiple bank accounts and manual ledger matching. The growth would have been operationally painful.

Mark: Strata and Rental Mix

Mark manages both strata bodies and rental portfolios.

Client A uses Amex rewards to fund annual Christmas events for tenants.

Client B uses NAB cashback to offset BAS lodgement fees.

Under a single bank account system, these funds would blend together, increasing audit exposure and reducing clarity.

Card splits allow clean entity dashboards per client.

This is how you scale bookkeeper clients card float strategy without chaos.

Comparison Table: Multi-Client Reality

Metric | Single Bank Account | Lessn Card Splits |

$120,000 across 7 clients | Day 1 drain | 55-day float per client |

Reconciliation | 127 manual lines | Auto merchant fee journal per ledger |

Client separation | High risk of mixing | Entity dashboards |

Scaling capacity | 7 clients maximum | 25 plus clients possible |

Monthly cashflow impact | -$468 cost | +$2,250 net reward |

Audit risk | High | Near zero with separation |

When viewed clearly, card splits vs single bank account is not about preference. It is about scalability and financial logic.

Implementation: Moving from 7 to 25 Clients

Week 1:

Connect Xero and configure seven client entities. Test a $5,000 pilot batch.

Week 2:

Introduce multi-card splits and train directors on SMS approval.

Week 3:

Scale to $200,000 per month. Automate merchant fee journals.

Month 2:

Onboard new Client H and Client I without adding admin hours.

Track metrics:

Client count growth

Batch volume increase

Reconciliation error rate

Approval time under 24 hours

With a 70 percent touch time reduction, you reclaim roughly 13 hours per week. That is capacity for 15 to 20 additional clients over time.

Conclusion

The single bank account model drains cash, caps growth, and creates reconciliation risk.

Card splits enable float, rewards, automation, and clean client separation.

For a multi client supplier payments bookkeeper, the numbers are not marginal. They are structural.

$120,000 per month can either cost you $468 and drain on day one.

Or generate $2,250 net, preserve 55-day float, and eliminate manual reconciliation across 127 invoices.

Upload your next multi-client batch and see the difference live.

FAQ

Can I use one bank account for seven clients safely?

Yes, but mixing ledgers increases audit risk and reconciliation complexity. Card splits maintain separation automatically.

Do client suppliers know I am using credit cards?

No. Suppliers receive standard EFT payments. Card funding happens behind the scenes.

Are card rewards taxable income for bookkeepers?

Reward points are generally not taxable, while merchant fees are tax deductible. Always confirm with your tax adviser.

What is the breakeven point for cards vs bank?

Typically above $5,000 per client monthly volume, float and rewards outweigh fees.

Does Xero auto-match multi-client card payments?Yes. Merchant fees are automatically journalled to the correct client ledger.

Continue Reading

START REWARDING YOUR HARD WORK TODAY

Join Australian businesses turning payments into rewards.